8 December, 2023

Using Machine Learning to Optimize Entries

During the week, I found a superbly helpful 'Machine Learning in Finance' guide on X that used clustering to group price behavior into different groups.

Here is a link to the clustering code by Danny Groves.

Like many educational insights on X (in particular), I typically bookmark to save for later and often forget to check. So, in an effort to change that,

I thought I would set myself the challenge of playing around with Danny's code and seeing a) what I could add and b) how I might tie it to something I have built in the past.

The strategy below takes the MA Crossover with ATR Trailing Stop Strategy and uses ML to increase the proability of successful entries. Basically, I took the cluster approach,

identified the three clusters that ranked best as a function of high returns and low volatility, and only entered trades when the MA crossover was within one of these

three 'good_clusters'. Instead of then trying to predict where price would go post-entry, I kept the regular ATR trailing stop approach that adjusts with increasing price.

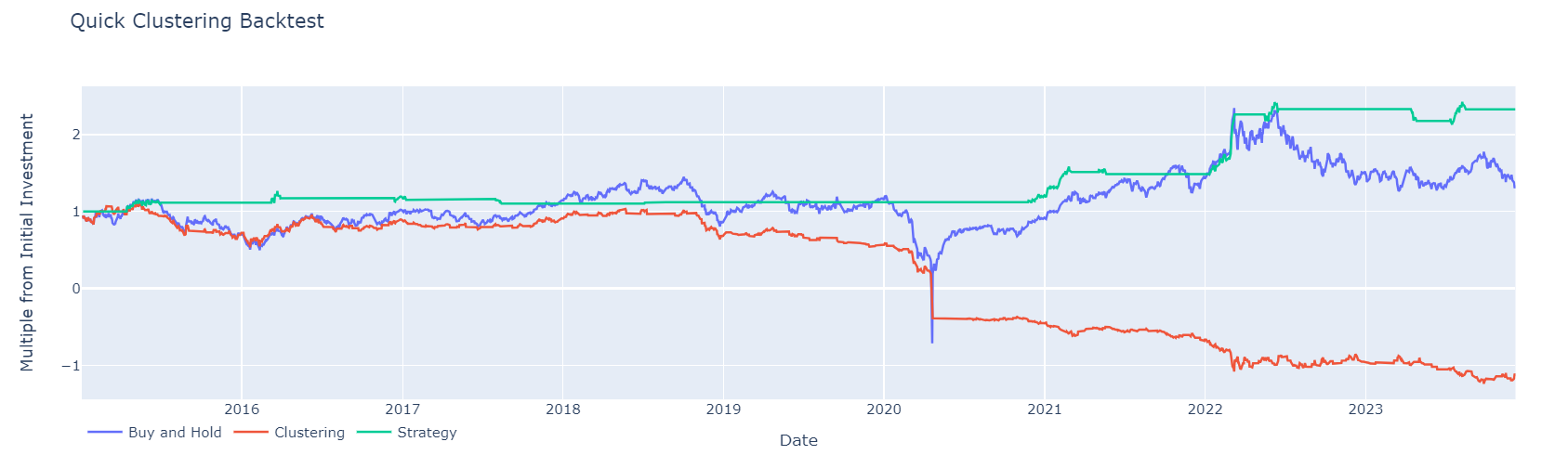

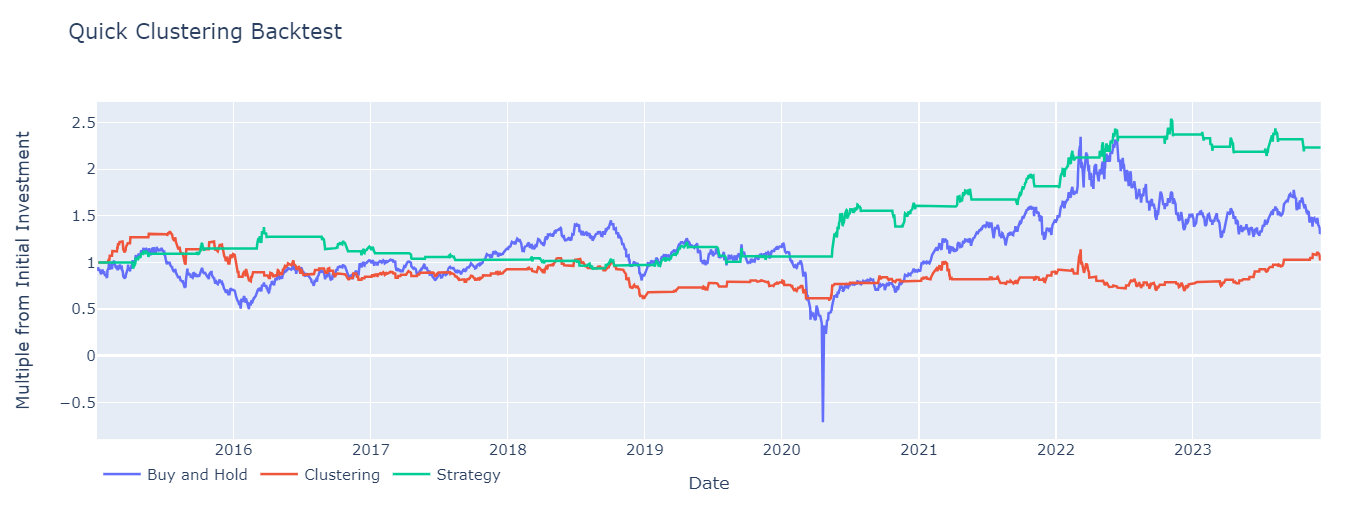

The results (when tested on OIL futures) are quite good: lowest drawdown and highest return. When I tested on other stocks/futures (SPY, GC=F, BTC-USD),

the results aren't as strong. In some cases, the clustering algorithm alone performs better - it all depends on the length of training data, the ATR multiplier chosen and the

Moving Average lengths.

My next post will compare how this model performs in different markets and environments.

(For simplicity sake, this is a long-only strategy and ignores any slippage, commisions etc.)

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import yfinance as yf

from sklearn.cluster import KMeans

from kneed import KneeLocator

from sklearn.ensemble import RandomForestClassifier

from sklearn.metrics import accuracy_score, precision_score, confusion_matrix

from sklearn.preprocessing import StandardScaler

import seaborn as sns

import plotly.express as px

from plotly import graph_objects as go

import yfinance as yf

import numpy as np

# Download SPY df

df = yf.download('CL=F').reset_index()

# Distance from the moving averages

for m in [10, 20, 30, 50, 100]:

df[f'feat_dist_from_ma_{m}'] = df['Close'] / df['Close'].rolling(m).mean() - 1

# Distance from n day max/min

for m in [3, 5, 10, 15, 20, 30, 50, 100]:

df[f'feat_dist_from_max_{m}'] = df['Close'] / df['High'].rolling(m).max() - 1

df[f'feat_dist_from_min_{m}'] = df['Close'] / df['Low'].rolling(m).min() - 1

# Price distance

for m in [1, 2, 3, 4, 5, 10, 15, 20, 30, 50, 100]:

df[f'feat_price_dist_{m}'] = df['Close'] / df['Close'].shift(m) - 1

# Add EMA features

for m in [10, 20, 30, 50, 100]:

ema = df['Close'].ewm(span=m, adjust=False).mean()

df[f'feat_dist_from_ema_{m}'] = df['Close'] / ema - 1

# Drop NaN values created by rolling functions

df = df.dropna()

# Split the df into training and testing sets based on date

df_train = df[df['Date'] < '2015-01-01'].reset_index(drop=True)

df_test = df[df['Date'] >= '2015-01-01'].reset_index(drop=True)

print(df_train.columns)

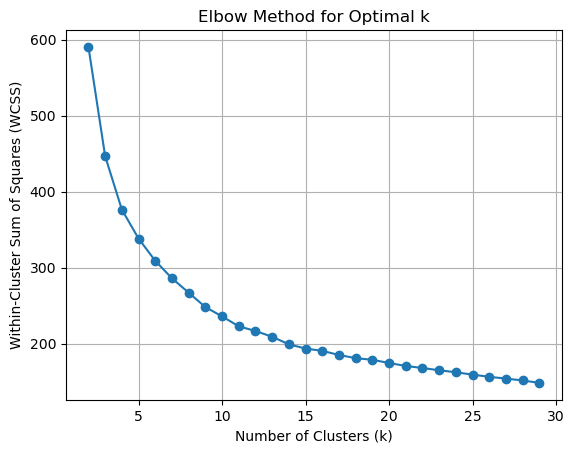

Next, we find the optimal number of clusters to work with. This is important because if we have too many clusters, many will be almost identical. By visually inspecting where WSS curve flattens or by using predict function, we can find optimal number of clusters to work with.

feat_cols = [col for col in df.columns if 'feat' in col]

X_train = df_train[feat_cols]

# List to store the within-cluster sum of squares for different k values

wcss = []

k_range = range(2, 30)

# Calculate WCSS for a range of k values

for k in k_range:

kmeans = KMeans(n_clusters=k, random_state=42, n_init='auto')

kmeans.fit(X_train)

wcss.append(kmeans.inertia_)

# Use KneeLocator to find the elbow point in the WCSS curve

elbow_locator = KneeLocator(k_range, wcss, curve='convex', direction='decreasing')

optimal_k = elbow_locator.elbow

print(f'Optimal k: {optimal_k}')

# Plotting the elbow curve

plt.plot(k_range, wcss, marker='o')

plt.title('Elbow Method for Optimal k')

plt.xlabel('Number of Clusters (k)')

plt.ylabel('Within-Cluster Sum of Squares (WCSS)')

plt.grid(True)

plt.show()

# Create a KMeans instance with the optimal number of clusters

optimal_kmeans = KMeans(n_clusters=optimal_k, random_state=42, n_init='auto')

optimal_kmeans.fit(X_train)

# Predict the clusters for the observations

df_train['cluster'] = optimal_kmeans.predict(X_train)

Optimal k: 9

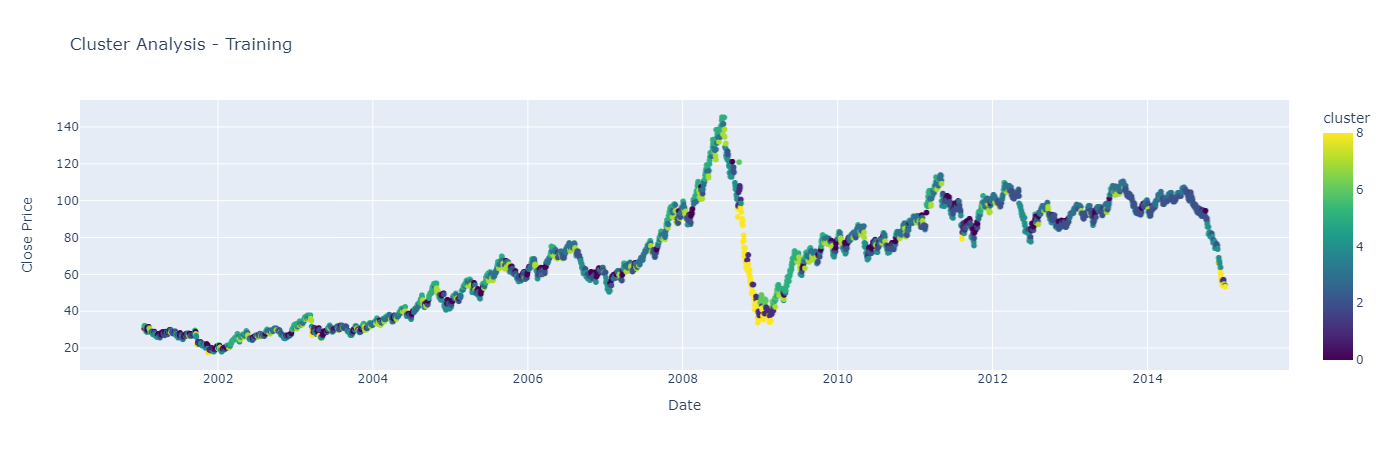

By visualizing the clusters, we can see which ones perform well in strong positive market environments

# Standardize features

scaler = StandardScaler()

df_scaled = scaler.fit_transform(df_train[feat_cols])

# Fit the KMeans model with the number of clusters as seen in the image (6 clusters)

kmeans = KMeans(n_clusters=10, random_state=42)

df_train['cluster'] = kmeans.fit_predict(df_scaled)

# Create a scatter plot using plotly express

fig = px.scatter(df_train, x='Date', y='Close', color='cluster',

title="Cluster Analysis - Training",

labels={'Close': 'Close Price'}, color_continuous_scale='Viridis')

fig.show()

While visually inspecting clusters, I find it important too to reaffirm what we believe by finding optimal clusters as a function of high returns and low volatility.

# Calculating daily returns

df_train['daily_return'] = df_train['Close'].pct_change()

# Grouping by cluster and calculating the mean daily return for each cluster

mean_cluster_returns = df_train.groupby('cluster')['daily_return'].mean()

# Calculating standard deviation (volatility) for each cluster

cluster_volatility = df_train.groupby('cluster')['daily_return'].std()

# Combining the returns and volatility into a single DataFrame

cluster_performance = pd.DataFrame({

'return': mean_cluster_returns,

'volatility': cluster_volatility

})

# Ranking clusters based on high returns and low volatility

# Lower rank is better for volatility, higher rank is better for returns

cluster_performance['return_rank'] = cluster_performance['return'].rank(ascending=False)

cluster_performance['volatility_rank'] = cluster_performance['volatility'].rank(ascending=True)

# Overall score to identify top clusters - lower score is better

cluster_performance['score'] = cluster_performance['return_rank'] + cluster_performance['volatility_rank']

# Selecting top 3 clusters based on the combined score

top_clusters = cluster_performance.nsmallest(3, 'score').index.tolist()

print(f"Top 3 clusters for the strategy: {top_clusters}")

Top 3 clusters for the strategy: [0, 2, 3]

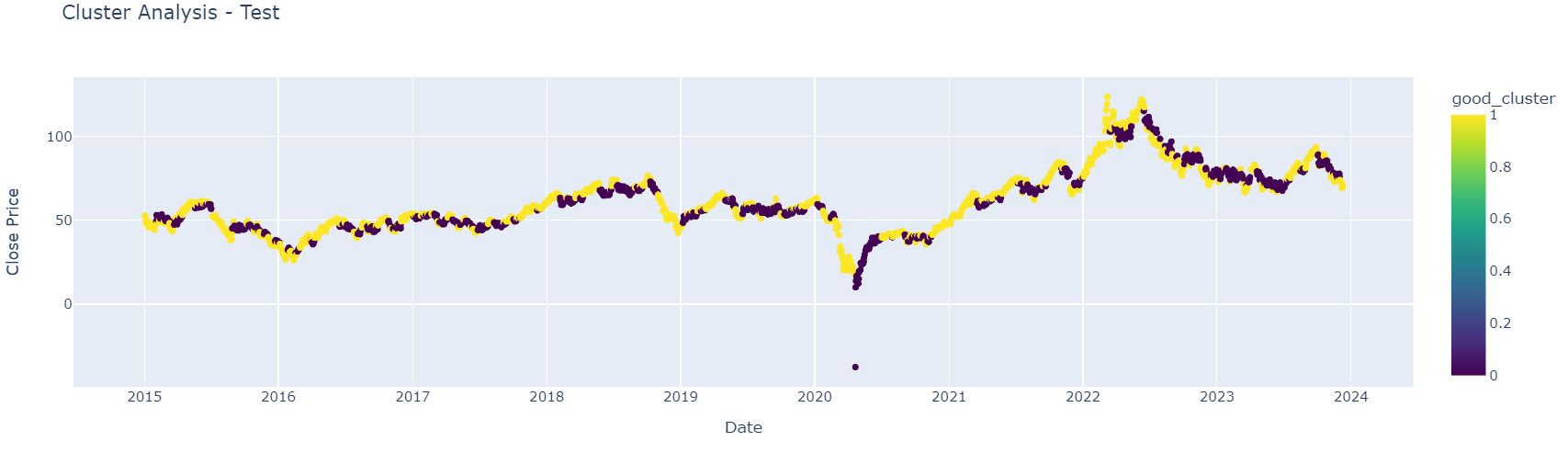

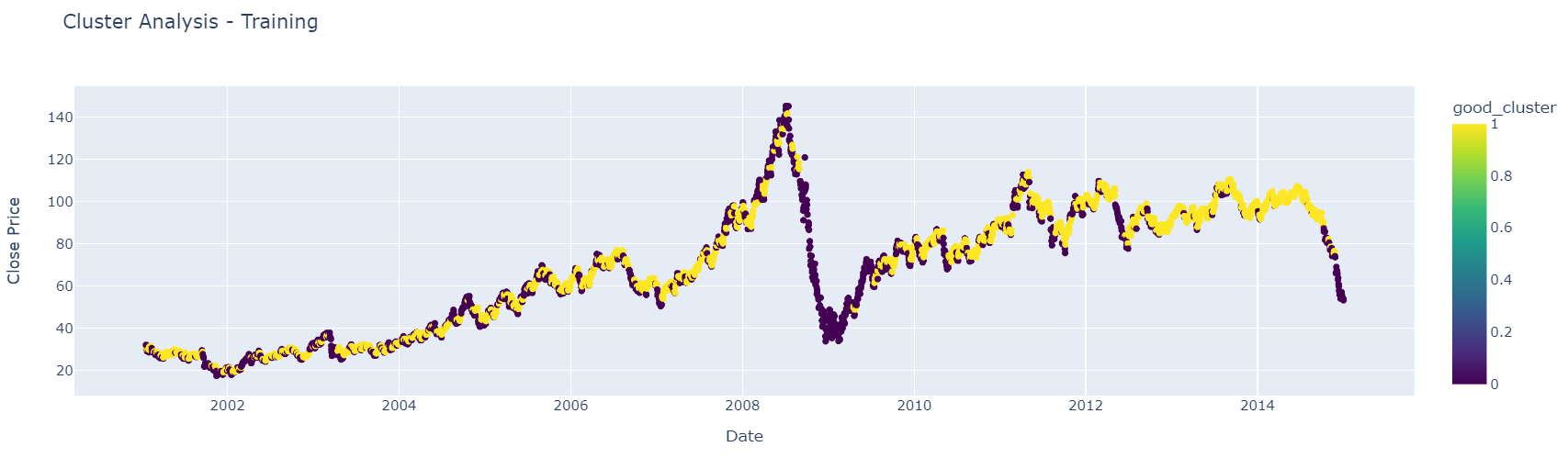

Then, to see if we do have a workable system, good clusters and bad clusters are grouped together into two different groups. First, we see how it looks on training data and then on test data.

# For visualization, classify clusters into 'good' and 'bad' based on the user's input.

good_clusters = [0, 2, 3]

df_scaled = scaler.fit_transform(df_train[feat_cols])

df_train['cluster'] = kmeans.fit_predict(df_scaled)

# Map the clusters to good and bad

df_train['good_cluster'] = df_train['cluster'].apply(lambda x: 1 if x in good_clusters else 0.0)

# Create a scatter plot using plotly express

fig = px.scatter(df_train, x='Date', y='Close', color='good_cluster',

title="Cluster Analysis - Test",

labels={'Close': 'Close Price'}, color_continuous_scale=px.colors.sequential.Viridis)

fig.show()

# Standardize features

scaler = StandardScaler()

df_scaled = scaler.fit_transform(df_test[feat_cols])

# Fit the KMeans model with the number of clusters as seen in the image (6 clusters)

kmeans = KMeans(n_clusters=9, random_state=42)

df_test['cluster'] = kmeans.fit_predict(df_scaled)

# Create a scatter plot using plotly express

fig = px.scatter(df_test, x='Date', y='Close', color='cluster',

title="Cluster Analysis - Test",

labels={'Close': 'Close Price'}, color_continuous_scale='Viridis')

fig.show()

The strategy remains almost identical (minus the shorting) as in my previous post with the addition of the 'good_cluster' check within the entry logic.

# Calculating moving averages

df_test['MA50'] = df_test['Close'].rolling(window=50).mean()

df_test['MA20'] = df_test['Close'].rolling(window=10).mean()

df_test['cluster'] = kmeans.fit_predict(df_scaled)

df_test['good_cluster'] = df_test['cluster'].apply(lambda x: 1 if x in good_clusters else 0.0)

# Function to calculate Average True Range (ATR)

def calculate_atr(df_test, period=21):

df_test['high_low'] = df_test['Close'].diff()

df_test['high_close'] = np.abs(df_test['Close'] - df_test['Close'].shift())

df_test['low_close'] = np.abs(df_test['Close'] - df_test['Close'].shift())

df_test['tr'] = df_test[['high_low', 'high_close', 'low_close']].max(axis=1)

atr = df_test['tr'].rolling(window=period).mean()

return atr

# Calculating ATR

df_test['ATR'] = calculate_atr(df_test)

# Setting the ATR multiplier

atr_multiplier = 3

# Identifying entry points for both long and short positions

df_test['Entry_Signal_Long'] = np.where((df_test['MA20'] > df_test['MA50']) & (df_test['MA20'].shift(1) <= df_test['MA50'].shift(1)), 1, 0)

df_test['Entry_Signal_Short'] = np.where((df_test['MA20'] < df_test['MA50']) & (df_test['MA20'].shift(1) >= df_test['MA50'].shift(1)), 1, 0)

# Initialize columns for position and trailing stop

df_test['In_Position'] = 0

df_test['Adjusted_Trailing_Stop'] = np.nan

# Variables to track position, trailing stop, and exit points

in_position = False

trailing_stop = 0

position_type = None

exit_points = []

trades = []

current_trade = {'Entry': None, 'Exit': None}

# Looping through the df_test to adjust position, trailing stop logic, and identify exit points

for index, row in df_test.iterrows():

if row['Entry_Signal_Long'] == 1 and not in_position and row['good_cluster'] == 1:

trailing_stop = row['Close'] - (row['ATR'] * atr_multiplier)

current_trade['Entry'] = (index, row['Close'])

in_position = True

position_type = 'long'

if in_position:

if position_type == 'long':

current_trailing_stop = row['Close'] - (row['ATR'] * atr_multiplier)

trailing_stop = max(trailing_stop, current_trailing_stop)

# Exit conditions

if (position_type == 'long' and row['Close'] < trailing_stop):# or (position_type == 'short' and row['Close'] > trailing_stop):

in_position = False

exit_points.append(index)

current_trade['Exit'] = (index, row['Close'])

trades.append(current_trade)

current_trade = {'Entry': None, 'Exit': None}

df_test.at[index, 'Adjusted_Trailing_Stop'] = np.nan

else:

df_test.at[index, 'Adjusted_Trailing_Stop'] = trailing_stop

else:

df_test.at[index, 'Adjusted_Trailing_Stop'] = np.nan

df_test.at[index, 'In_Position'] = int(in_position)

# Applying fillna() to ensure trailing stop is only plotted when in a position

df_test['Plot_Trailing_Stop'] = df_test['Adjusted_Trailing_Stop'].where(df_test['In_Position'] == 1)

from plotly import graph_objects as go

import numpy as np

df_test['pct_change'] = df_test['Close'].pct_change()

df_test['signal'] = df_test['good_cluster'].shift(1)

df_test['equity_cluster'] = np.cumprod(1+df_test['signal']*df_test['pct_change'])

df_test['equity_buy_and_hold'] = np.cumprod(1+df_test['pct_change'])

# Calculate the cumulative product of equity for the strategy

df_test['In_Position'] = df_test['In_Position'].shift(1)

df_test['equity_strategy'] = np.cumprod(1 + df_test['In_Position'] * df_test['pct_change'])

fig = go.Figure()

fig.add_trace(

go.Line(x=df_test['Date'], y=df_test['equity_buy_and_hold'], name='Buy and Hold')

)

fig.add_trace(

go.Line(x=df_test['Date'], y=df_test['equity_cluster'], name='Clustering')

)

fig.add_trace(

go.Line(x=df_test['Date'], y=df_test['equity_strategy'], name='Strategy')

)

fig.update_layout(

title_text='Quick Clustering Backtest',

legend={'x': 0, 'y':-0.05, 'orientation': 'h'},

xaxis={'title': 'Date'},

yaxis={'title': 'Multiple from Initial Investment'}

)

def get_max_drawdown(col):

drawdown = col / col.cummax() - 1

return 100 * drawdown.min()

def calculate_cagr(col, n_years):

cagr = (col.values[-1] / col.values[0]) ** (1 / n_years) - 1

return 100 * cagr

print('Maximum Drawdown Buy and Hold:', get_max_drawdown(df_test['equity_buy_and_hold']))

print('Maximum Drawdown Clustering:', get_max_drawdown(df_test['equity_cluster']))

print('Maximum Drawdown Strategy:', get_max_drawdown(df_test['equity_strategy']))

print('')

n_years = (df_test['Date'].max() - df_test['Date'].min()).days / 365.25

print('CAGR Buy and Hold:', calculate_cagr(df_test['equity_buy_and_hold'].dropna(), n_years))

print('CAGR Clustering:', calculate_cagr(df_test['equity_cluster'].dropna(), n_years))

print('CAGR Random Strategy:', calculate_cagr(df_test['equity_strategy'].dropna(), n_years))

Maximum Drawdown Buy and Hold: -149.24747973382892

Maximum Drawdown Clustering: -55.67676221505267

Maximum Drawdown Strategy: -32.73684867226392

CAGR Buy and Hold: 4.037706652182704

CAGR Clustering: 0.6633401650248505

CAGR Random Strategy: 9.41790316427702